The environmental risks from a critical minerals rush in Ukraine

Published: May, 2024 · Categories: Publications, Ukraine

Since February 2022, Ukraine has sought to attract international investment and political partnerships by licensing critical mineral deposits. In this analysis, Iryna Babanina and Rob Watson examine how the demands of the conflict, economy and recovery are exacerbating the threats that their exploitation could pose for Ukraine’s environment.

Contents

Critical minerals in Ukraine

Background

In contrast to most European countries, Ukraine hosts a wide variety of critical mineral deposits and is increasingly examining their potential to support its economic recovery. Critical minerals refer to the elements necessary to produce the chips and batteries found in high-tech devices such as smartphones and laptops. They are also essential for the manufacturing of renewable energy technologies such as wind turbines, electric vehicles and solar panels.1

In spite of their global importance,2 supplies of critical minerals are at risk of disruption due to the concentrated nature of their extraction and production. Some such as copper are relatively widespread,3 whereas others such as cobalt can only be found in a few places at economic concentrations.4 Furthermore, whilst the distribution of critical mineral deposits varies, their processing is currently concentrated in China.5 This means that events like the COVID-19 pandemic can expose supply chains to disruption.6

These risks and geopolitical imbalances have increased attention on developing sources closer to key markets such as Europe, and it is in this context that the critical mineral resources of Ukraine have attracted increased global interest.

The location and status of Ukraine’s critical mineral deposits

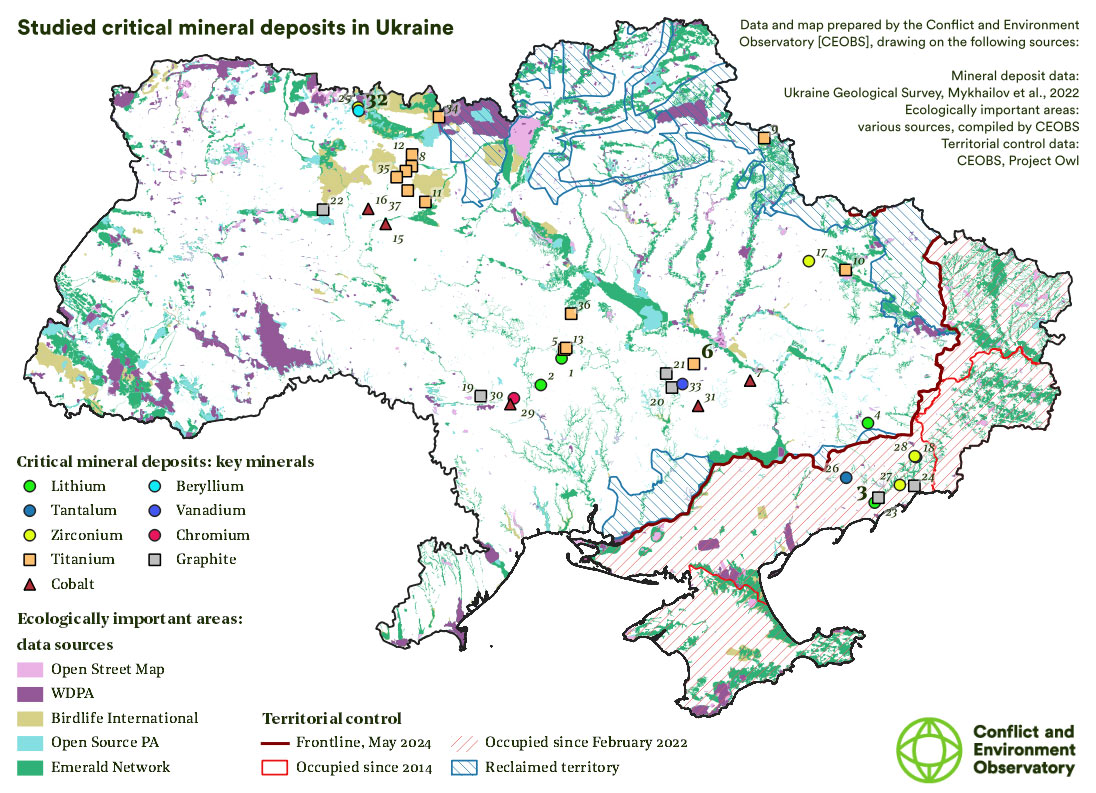

We mapped the locations of 37 critical mineral deposits in Ukraine using publicly available information.7 Of these 11 are already operational, seven have been licensed to mining companies – although extraction has not yet begun, and the remaining 19 are ready for auction. Where possible, we also obtained information on their licence holders.

| Site name | ID | Location confidence | Key mineral | Additional minerals | Exploration status |

|---|---|---|---|---|---|

| Polokhivske | 1 | High | Lithium | Licensed | |

| Dobra | 2 | High | Lithium | Scandium, tantalum, niobium, rubidium, tin, caesium | Licensed |

| Kruta Balka | 3 | High | Lithium | Beryllium, tantalum, niobium, rubidium, tin caesium | Auction-ready |

| Shevchenkivske | 4 | High | Lithium | Licensed | |

| Birzulivske | 5 | High | Titanium | Operational | |

| Malyshivske | 6 | High | Titanium | Zirconium | Operational |

| Karnaukhivska | 7 | High | Cobalt | Nickel | Auction-ready |

| Selyshchanska | 8 | High | Titanium | Licensed | |

| Korchakiv | 9 | High | Titanium | Zirconium | Auction-ready |

| Haydariv | 10 | High | Titanium | Zirconium | Auction-ready |

| Pidlisna | 11 | High | Titanium | Zirconium | Auction-ready |

| Stremyhorod | 12 | Moderate | Titanium | Scandium, vanadium, apatite | Operational |

| Likarivske | 13 | Low | Titanium | Licensed | |

| Mezhyrichne | 14 | Moderate | Titanium | Operational | |

| Zhelezniaky | 15 | Moderate | Cobalt | Nickel, copper | Auction-ready |

| Prutivskyi | 16 | Low | Cobalt | Copper, nickel, platinium group metals | Licensed |

| Zolochivska | 17 | Low | Zirconium | Titanium | Auction-ready |

| Mazurivske East | 18 | High | Tantalum | Niobium, zirconium, rare earth elements (REEs) | Operational |

| Zavallivske | 19 | High | Graphite | Operational | |

| Petrivske | 20 | High | Graphite | Operational | |

| Balakhivske | 21 | Low | Graphite | Operational | |

| Burtynske | 22 | Low | Graphite | Operational | |

| Troitske | 23 | Low | Graphite | Auction-ready | |

| Mariupilske | 24 | Low | Graphite | Auction-ready | |

| Yastrubetske | 25 | Moderate | Zirconium | REEs | Licensed |

| Novopoltavske | 26 | High | Tantalum | Niobium, REEs | Auction-ready |

| Azovske | 27 | Low | Zirconium | REEs | Auction-ready |

| Mazurivske North | 28 | High | Zirconium | Niobium | Auction-ready |

| Kapitanivske | 29 | High | Chromium | Nickel, cobalt | Operational |

| Ternuvatske | 30 | Low | Cobalt | Nickel | Auction-ready |

| Devlad?vske | 31 | Low | Cobalt | Nickel | Auction-ready |

| Perzhansk | 32 | High | Beryllium | Tantalum, niobium, zirconium | Operational |

| Zhtorichenske | 33 | Low | Vanadium | Scandium, titanium | Auction-ready |

| Davydkivske | 34 | Low | Titanium | Auction-ready | |

| Kropyvnyanskoe | 35 | Moderate | Titanium | Auction-ready | |

| Nosachivske | 36 | Low | Titanium | Auction-ready | |

| Fedorivske | 37 | Low | Titanium | Vanadium | Auction-ready |

All the lithium deposits in territory still controlled by Ukraine have been licensed for exploitation. The Polokhivske deposit (deposit 1) has been licensed to ULM, a Ukrainian lithium mining company. ULM is lobbying internationally for further outside investment because the deposit is complex and extraction will be costly.

Foreign investors include the Australian mining company European Lithium, which already has operations in Austria, and which claims to be ‘ready to invest $1bn in lithium mining in Ukraine’. The company has provisionally obtained the licences to mine at Shevchenkivske (deposit 4), which is located only a few kilometres from the present frontline, and at Dobra (deposit 2) where lithium ores occur alongside a deposit of rare earth elements (REE) including tantalum, niobium, rubidium and cesium. The licence for Dobra was bought from a Ukrainian company PetroConsulting LLC in 2023.8

Elsewhere, Turkey’s Onur Group has invested $50m to mine graphite at the Burtynske site (deposit 22), and controls seven other mining assets in Ukraine. Another Australian company, Volt Resources, has acquired the rights to mine graphite at Zavallivske (deposit 19) until 2035. Volt showcased its plans for the deposit in London in June 2023 at a meeting on the planned Ukraine-EU strategic partnership for critical mineral mining.

Velta LLC, a joint Ukrainian-US venture, has been developing the Birzulivske site (deposit 5) since 2006, and has also obtained a licence to mine titanium at the Likarivske deposit (deposit 13). It also operates the largest titanium processing facility in Ukraine. However, it is the Ukrainian-US BGV Group that has the largest and most diverse stake in Ukraine’s critical minerals. BGV has obtained licences to mine major deposits of graphite at the Balakhivske deposit (deposit 21); zirconium and REEs at the Yastrubetske deposit (deposit 25); and beryllium at the Perzhanske deposit (deposit 32). Concerns have been raised over the process through which BGV obtained the permit to mine at Perzhanske.

Occupied deposits

Of the 37 deposits we examined, seven are in territories occupied by Russia since 2022. These include the Kruta Balka lithium deposit; the Mazurivske deposits, which are rich in tantalum, zirconium, niobium and other REEs; and the graphite deposits at Troitske and Mariupilske. As noted above, the strategic Shevchenkivske lithium deposit near Donetsk is located close to the frontline.

The extent to which control over Ukraine’s confirmed deposits of critical minerals, as well as its gas reserves, has played a role in Russia’s strategic calculus since 2014 has been discussed. At the peak of the occupation in 2022 it was estimated that more than $12tn of Ukraine’s natural resources were under Russian control. More recently it has been suggested that Russia plans to exploit resources under its control to help fund the war.

Exploiting the occupied deposits would not be straightforward. Only one – the niobium and zirconium mine at Mazurivske East – was operational before February 2022. Russia would need to make significant investments in both infrastructure and personnel to exploit the remainder. While Russian legislation includes a form of environmental impact assessment and a procedure called a ‘governmental/state environmental review’ – any research to inform it, and any subsequent decisions made, will be made under political pressure and thus risking their integrity. Legitimate public participation in the process is unlikely. More profoundly, Russia’s exploitation of Ukraine’s mineral resources in areas under occupation for the benefit of its coffers would likely constitute the crime of pillage.

Impact of the full-scale invasion on critical mineral exploitation in Ukraine

The overall effect of the invasion has been to stall the development of Ukraine’s critical mineral deposits. Investors are wary of committing to projects in Ukraine, while the Ukrainian state does not have the funds spare to develop the infrastructure to exploit many of them. Indeed, existing critical mineral exports have been hampered by the conflict’s constraints on sea and rail transport, even as domestic demand for critical minerals such as titanium, which has numerous military applications, has grown.

However, preparations for extraction at scale for international markets after the war ends have accelerated, having begun with the signing of a Memorandum of Understanding on raw materials between Ukraine and the EU in July 2021. The EU is seeking to ‘onshore’ production and develop new strategic ties to reduce reliance on Chinese imports. In November 2022, the Ukrainian Geological Survey signed a partnership with the European Bank of Reconstruction and Development, to digitise geological data and translate historical prospecting and survey documents into English. Changes were subsequently made to simplify and accelerate Ukraine’s procedures for environmental impact assessments. The EU’s Critical Raw Materials Act, passed into law in March 2024, further cemented these ties.

Ukraine’s government is encouraging foreign investment in its subsoils; meetings took place throughout 2023, including at the Ukraine Recovery Conference. Ukrainian law firms have provided strategic and legal guidance for investors and interest is growing. In 2023 the Ukrainian government granted more than 400 special permits to exploit subsoil, a 10% increase from 2021. The state revenue raised through these permits amounted to UAH2.3bn – around $60m.

The environmental risks from critical mineral exploitation in Ukraine

Economic interests commonly trump environmental considerations during and after conflicts, and this rush to exploit Ukraine’s critical mineral deposits has triggered fears that the country’s ecosystems may suffer as a result. This in the context of historical degradation from industry and intensive agriculture, as well as the more recent damage linked to the ongoing conflict.

The environmental impacts of mining are extensive and diverse. They can include land degradation and soil erosion,9 subsidence,10 polluting mine drainage into aquifers,11 landform destruction,12 and the contamination of soils, surface and ground waters from mine tailings.13

The threat of water pollution by acid mine drainage from the inadequate management of mine tailings is already of particular concern in Ukraine; a threat being exacerbated by the conflict. Tailings management will also be a key challenge for the mining industry and Ukrainian state if new critical mineral deposits are exploited as part of rebuilding efforts.14

The environmental legacy of mining in Ukraine is already substantial and the exploitation of new deposits risks damaging environmentally sensitive areas. Of the 37 critical mineral sites we examined:15

- 19 deposits are within 1 km of an Ecologically Important Area (EIA);

- 7 deposits are within 100 m of an EIA;

- 18 deposits are within 1 km of a surface water body (river, stream or lake);

- 5 deposits are within 100 m of a surface water body.

Development of these prospective sites has the potential to impact wetlands and rivers, old-growth forest and steppe. Where mining instead occurs in agricultural areas, this can encourage the conversion of unprotected land to agricultural uses to compensate. The authorities have already stated their intention to convert such ‘rear’ regions to make up the shortfall.

We analysed the potential environmental impacts of mining at three representative sites.

Kruta Balka deposit – deposit 3

Kruta Balka is a complex REE deposit in an area that has been occupied by Russia since 2022. In addition to lithium, the deposit contains tantalum, niobium, beryllium, tin, caesium and rubidium; this makes it a lucrative mining prospect. The proposed mining would occur within an Emerald Network site and would cross a close tributary of the River Berda.16 Mineral extraction would therefore likely result in the destruction of multiple threatened and valuable ecosystems.17 It would also damage unique Precambrian geoheritage,18 and exacerbate existing water stress in the area.19

Malyshivske deposit – deposit 6

The Malyshivske titanium and zirconium deposit has been developed since 1961. In 2019 plans were published for a new ore refinement facility, transport terminal and two tailings ponds.20 Extraction was proposed to be expanded by up to 2.7 million m3 of ore-rich sands per year over the next 60 years.

This would vastly increase the volume of mine waste to be managed in the vicinity of several surface watercourses in what is a highly productive agricultural area.21 It would also exploit and disturb aquifers that are likely to become important sources of water in the future.22

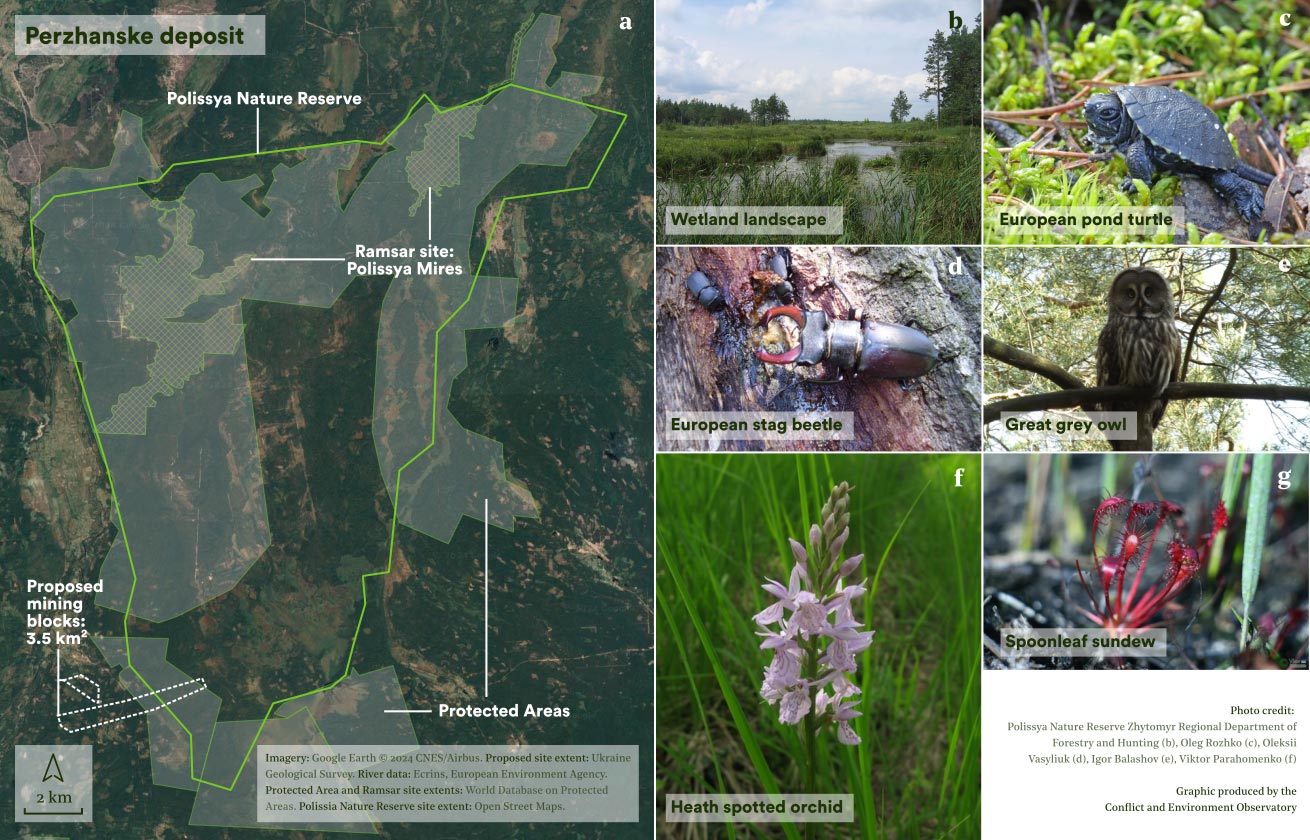

Perzhanske deposit – deposit 32

The Perzhanske deposit contains beryllium and REEs. It was discovered in the early 1950s and mined historically until 1977.23 Renewed mining at this site would endanger a rich and varied network of ecosystems at the confluence of several designated EIAs within the wider Polissya wilderness, which is often referred to as ‘Europe’s Amazon’.

Part of the proposed mining area is located within the Polissya Nature Reserve, where mining is still prohibited; however, other adjacent areas are not equally protected.24 The forests and wetlands are rich in biodiversity. Animal species include mammals such as beavers, moose and wolves, and birds like the great grey owl and the arctic loon, along with threatened species such as the European lynx, the European stag beetle and the European pond turtle. The wetlands are important carbon sinks, and beryllium mining poses severe risks to these aquatic ecosystems.25 The proximity of Polissya to the Belarusian border has also highlighted the effects of war on wildlife and conservation work in the reserve.

Safeguards or sacrifice? Tensions in environmental protection

The accelerating onshoring of critical mineral extraction in the EU is resulting in conflicts and confrontations that have parallels to those in countries where critical mineral exploitation has been ongoing for many years. There is concern that this onshoring will further entrench existing environmental inequities, in some cases by exploiting weaker regulative structures than those that exist within the EU;26 in effect ‘offshoring’ the environmental harms whilst securing EU access to critical minerals.

For Ukraine, it is now a question of whether it can balance effective mining governance with the levels of responsible mining necessary to support its economic recovery as part of the global energy transition.

Ukraine already has legislative safeguards intended to limit the environmental impact of mining. Provisions of its Land Code bind legal entities or individuals to rehabilitate land damaged by their activities.27 The Law on Land Protection imposes requirements to protect fertile topsoil.28 Article 50 of the Subsoil Code establishes that environmental safety measures and land rehabilitation must be a part of projects to develop deposits or to build processing facilities. The law on Product Distribution Agreements envisages land rehabilitation projects, while permits for subsoil use contain requirements to protect the natural and built environments.

Prior to February 2022, compliance with environmental legislation and the state’s ability to enforce it were poor. This was attracting new legal instruments, including laws seeking to limit industrial activities in Emerald Network sites, which had been debated in parliament but repeatedly blocked. Some questioned whether such laws would be effective. Others opposed them because they feared they would be used to exert political pressure, a reminder that official oversight and enforcement must be transparent and explicit.

Since the full-scale invasion, mining legislation has been overhauled to attract investors. Their environmental protections have been rolled back, even as corporations involved in some of the new critical mineral mining projects have sought to enhance their public image by selling their ESG credentials.29

In July 2023, amendments were made to the law on environmental impact assessments, whose procedures broadly match those of the EU. The law covers most types of mining projects and was amended to shorten the timeframe for public consultation, while introducing additional consultations with relevant state and local authorities.30 At present, other restrictions associated with martial law further limit public participation in environmental decision-making.31

This gives local authorities a greater say over the final decision than the public. In Ukraine, local authorities collect 5% of the subsoil use fee for the mining of ‘mineral resources of national importance’, which include non-ferrous ores and REEs.32 They also receive 25% of all environmental taxes levied as compensation for soil, air and water pollution. Ukraine’s local authorities face huge financial shortfalls as a result of the conflict and may be motivated to agree to potentially harmful projects to weather economic difficulties or raise money for restoration.

Given the environmental destruction that licensed mining activities have already caused in Ukraine, and the growing international thirst for critical minerals, increased public scrutiny and pressure will be required to protect its environment, both now and once peace returns. As the ultimate market for many of Ukraine’s critical minerals, the EU also has an obligation to ensure that its thirst for them does not contribute further to Ukraine’s environmental problems.

Rob Watson and Iryna Babanina are Junior Researchers at CEOBS. We acknowledge Dariia Borovyk and Denys Vynokurov for kindly providing photos of plant communities in the Berda River valley, and Oleg Rozhko, Oleksii Vasyliuk, Igor Balashov and Viktor Parahomenko for making their photos publicly available on iNaturalist.

Further reading

Exploration and mining perspectives of the critical elements for green technologies in Ukraine | Mykhailov et al., 2022

Prospects of development of lithium resource base in Ukraine | Vasylenko and Naumenko, 2022

Ukraine Recovery Conference Presentations, 21 – 22 June 2023, London | EU–UA Strategic Partnership on Raw Materials

Reform of the Ukrainian Raw Materials Sector | Ukraine Geological Survey

Why Did Ukraine Score Lowest in European Environmental Compliance? | Vox Ukraine

Guide to rebuilding Ukraine — Mining and extraction | Aequo

Five key trends in the development of Ukraine’s mining industry in 2023 | GMK Center

Sacrifice zones for sustainability? Green extractivism and the struggle for a just transition | European Environmental Bureau

- The definition of critical minerals has evolved over time, and the list of minerals that are considered ‘critical’ varies somewhat from country to country, depending on their geographic availability and projected future demand. In 2011, the EU’s list of critical minerals contained only 14 elements. Now in its fifth iteration, the 2023 list contains 34. Examples of critical minerals and their uses include but are not limited to: Lithium: Used in batteries for electric vehicles and energy storage. Cobalt: A key component in lithium-ion batteries. Graphite: Used in battery anodes and various industrial applications. Tungsten: Important for high-strength materials and industrial applications. Antimony: Used in flame retardants and semiconductors. Indium: Essential for touchscreens and thin-film solar cells. Gallium: Used in semiconductors and LEDs. Rare earth elements (REEs): These are a sub-group of 17 elements crucial for electronics, permanent magnets used in wind turbines and EV motors, and advanced technologies.

- According to the World Bank report Minerals for Climate Action, the demand for critical minerals just for energy needs is expected to double, triple, and for some, increase five-fold by 2050.

- Figures from 2022 show that Chile produces ~20% of global copper, with Australia at ~10% and the US at ~5%. No European country contributes any significant copper reserves to the global economy.

- Figures from 2022 indicate that ~70% of current cobalt production is located in the Democratic Republic of the Congo, with Indonesia and Russia the next largest at ~5% each. As with copper, no European country contributes any significant cobalt reserves.

- It’s estimated that 85% of REEs globally are sent to China for refining into usable materials.

- From 2020-22, lockdowns and restrictions in China resulted in a reduction in critical mineral supply and the manufacturing of semiconductors, which in turn led to a 16% slump in automobile production globally. The risks associated with the concentration of critical mineral production and processing are in many cases compounded by low substitution potential (inability to replace the mineral with anything else) and low recycling rates.

- We focused on certain groups of critical mineral deposits, depending on their commercial value and the ease of extraction: Critical mineral deposits that are already widely exploited in Ukraine (titanium, graphite). Critical mineral deposits that are in great demand globally, and specifically on the European market, which Ukraine has potential to develop at scale: lithium, beryllium, zirconium, scandium and vanadium. REEs are generally produced as secondary products when mining primarily for these deposits. Critical minerals that are unlikely to be economically viable for exploitation in Ukraine, despite the existence of deposits (cobalt). Copper and nickel are viewed by the EU as ‘Strategic Raw Materials’, and are generally found coincident with cobalt in the same deposits. We derived information on the physical limits of deposits, along with associated licence agreements, from collections of subsoil surveys held by the Ukrainian State Geological Survey, along with several presentations given by the Geological Survey and the companies investing in critical mineral extraction in Ukraine at conferences, and assorted other company websites and news articles.

- After buying an initial tranche of shares in Petro-Consulting in 2021, European Lithium tried to prevent another round of auctions for the subsoil permit at Dobra by applying for a ‘special permit’. This would have granted them the right to exploit the site without the licence going to auction; however, Ukraine’s courts ruled against European Lithium three times before they were eventually able to gain full control of the subsoil permit.

- The clearing of vast tracts of vegetation and construction of earthworks is widely reported for mining sites in tropical areas, with industrial mining leading to indirect deforestation in two-thirds of tropical countries, though direct deforestation is concentrated in only certain countries. The resulting soil erosion causes vast increases in sediment flux in surrounding rivers: one study measured an increase in suspended sediment of more than 200% in 15 years, which is strongly correlated with a 400% increase in mined areas for the region in the same period. Another study estimated that Brazil alone produced 3.6 gigatonnes of mining waste from 2008-19, which has affected ecosystems across the country as the sediment, dust and mud is dumped and then eroded and transported across boundaries. Furthermore, opencast nickel mining in Indonesia has been shown to significantly inhibit tree shoot growth due to reduced soil fertility. The loss of vegetation in mining areas increases the airborne dispersion of mining pollutants as well as discharges into rivers.

- Subsidence at active and abandoned mining sites can result from the collapse of overburden into underground quarries and shafts, along with widespread subsidence induced by dewatering and dissolution. These phenomena can result in extensive damage to property and loss of life, along with disruption of the prevailing geological and biological conditions of an area. See Bell et al., 2000, for an overview of the environmental impacts of mining subsidence, and see Parise, 2012, Mahboob et al., 2019, Guzy and Malinowska, 2020, and Bazaluk et al., 2023 for a non-exhaustive list of specific examples.

- Acid mine drainage, which occurs when sulphides and other heavy metals are oxygenated, is one of the most widely recognised environmental concerns arising from mining activity. The pollutants produced migrate across the natural environment and have bioaccumulative effects. Drainage hazards are especially pronounced in karst aquifers, as pollutants can be transported without buffering or attenuation for many kilometres from the pollution source.

- The removal of vast amounts of rock, and thus destruction of geodiversity, is an intrinsic part of the mining process. Mossa and James (2013) provide an overview of the geomorphological impacts of mining.

- The negative impacts of mine tailings on the environment are widely reported, exposing multiple ecosystems to highly toxic waste and collapse hazards. The waste products from critical mineral mining are generally considered to be of increased toxicity as compared to the waste products from mining for e.g. iron or steel.

- The amount of waste produced by a particular mining venture will vary depending on the nature of the deposit, the grade of the deposit and the specific mineral being mined. Critical mineral deposits are generally complex deposits and therefore generate high volumes of waste: for example, lithium mining generates between 20 – 40 tonnes of waste per tonne of product, while REE mining can generate up to 1 million tonnes of waste per tonne of product. The method of extraction also plays a role: open-cast mining typically generates six times as much solid waste as underground mining. Although to our knowledge numbers are not available for Ukraine, in Sweden, a country with similar geology and mineral deposits to Ukraine, the mining industry accounts for more than 80% of total annual solid waste products. Ukraine’s mining sector is nearly twice as productive as Sweden’s in terms of value ($13 billion in 2021 vs $7 billion for Sweden), so we can expect the volumes of waste generated by Ukrainian mining to be significantly larger in absolute terms, with this amount of waste very likely to increase if new critical mineral deposits are exploited.

- To analyse the current and potential environmental effects of critical mineral mining in Ukraine, we took the locations of the centres of the deposit extents and buffered these by 100 m and 1 km radially. Although polygon data is available for some of the studied deposits, we did not use these polygons in the analysis to maintain consistency: instead, our analysis takes a point approximately at the centre of the deposit and buffers it, rather than using a polygon of the deposit as these do not currently exist for all deposits analysed. We used the recently-compiled map of Ukraine’s Ecologically Important Areas (EIAs) to analyse the intersections between EIAs and critical mineral deposits. Additionally, we used surface water data from the Ecrins and European Environment Agency to analyse the proximity of the critical mineral sites to river courses and lakes.

- The Emerald Network is the network of the areas of special conservation interest aimed at protecting species and habitats of the Bern Convention. Even though a number of areas in Ukraine have successfully passed the biogeographical assessment, the national legislation regulating the Emerald sites management is not in place yet.

- The steppe and steppe-like grassland habitats surrounding the River Berda are a remnant of a once far more widespread zone of steppe grasslands. These environments were already in decline prior to the 2022 occupation by Russia. Aside from the immediate impacts to these grassland habitats within the Emerald Network site affected, pollution to the freshwater environment of the wider River Berda will put downstream sites at significant risk. The River Berda Mouth and its associated bay and spit are both Ramsar protected sites, and the Sea of Azov, into which the river flows, is already the site of decades of pollution and overexploitation. Any engineering solution to prevent immediate pollution of the river by diverting its course would certainly negatively affect populations of aquatic life in its waters.

- The Precambrian crystalline basement rocks in which the Kruta Balka deposit is formed have been proposed as a geoheritage site. The local area was the site of artisanal and small-scale mining historically, as evidenced by the many disused mine shafts and adits visible in satellite images and user photos on Google Earth. A resumption of mining at industrial scales would destroy this geoheritage: indeed, the application of modern industrial extraction to the adjacent Surozhske gold deposit has been discounted due to environmental concerns.

- Berdyanske Reservoir, located on the River Berda directly adjacent to the proposed deposit, serves as a backup water source for Berdyansk city, despite the fact that the water is unsuitable for domestic use due to high sulphite content and hardness. Before the destruction of the Kakhovka Dam, the city, with a population of about 100,000 people relied on Dnipro water supplied through the 175 km Western Group Aqueduct. The region’s water supply and irrigation systems have been considerably degraded during the Russian occupation. Aquifers in the Near Azov area are scarce and often highly mineralized, thus, any mining-related pollution will exacerbate the already severe water problem in the area.

- The environmental impact assessment (case registered under No. 20197174107) states that Motronivskyi Ore and Chemical Factory plan to construct an ore refinement facility with the capacity of 4.75 million tonnes/year and tailings ponds with volumes of 20 million m3 and 108 million m3 respectively.

- Our analysis of OSM data shows that the planned expansion of mining will directly remove at least 11 km2 of farmland from production, and occur within 100 m of four separate watercourses. The surrounding area is of highly fertile chernozem soils: if these currently productive agricultural areas are repurposed or their yields are negatively impacted by mining, then farming will need to expand into areas where it does not yet occur to meet demand.

- Known ore layers that are more than 90 m deep overlap with the Sarmathian artesian aquifers in the area, and the resulting drainage and pumping of these aquifers is likely to be exploited for industrial purposes. Local communities have centralised water supply, but of very poor quality. Therefore, these aquifers are of importance as a secondary drinking water supply, and possibly as a primary source of drinking water in the future, so their use in industrial settings is a source of renewed drinking water stress locally.

- The deposit contains quite a unique combination of ores such as zinc, tungsten, niobium, molybdenum, lithium, tin, germanium, cadmium, silver and tantalum. Its staple ores, genthelvite and phenakite, assessed to be about 2,835,700 tonnes, are considered to contain 13% BeO and 44% BeO respectively. Significant prospecting has already occurred in association with the site, which is managed by the BGV group.

- BGV Group argues that the nature reserve boundaries are not defined in any binding document and they would agree not to trespass on the protected area and buffer area land once those are defined. Attempts were made in the regional courts to block BGV from obtaining a special permit to mine in these areas, but they were ultimately unsuccessful. Similar tactics have been employed previously to try and gain approval for industrial amber mining in the region.

- Mining will cause groundwater drawdown and mine effluent management will be another problem because of residual beryllium content and an array of other elements with different mobility and toxicity patterns. Acute beryllium toxicity risk upon inhalation is well-studied. Beryllium and its compounds are believed to have severe chronic toxicity to aquatic life. While beryllium tends to be immobilised in soils in a non-bioavailable form, higher concentration may be found in wetland environments.

- One such example is in Serbia, where Rio Tinto had its licence to operate at the Jadar lithium deposit revoked due to widespread local protest; however, the Serbian government hopes to revive plans to exploit the deposit. Like Ukraine, Serbia is not an EU member state but is in negotiations to join, and also has less developed environmental regulations compared to EU member states.

- This specifically includes the rehabilitation of the lands that have their structure, geological characteristics or hydrological regime disrupted by mining exploration or deposit development works.

- While clearing a site, the fertile soil should be removed layer by layer, transferred to some already damaged or less valuable areas, and later the development site should be rehabilitated in a way that restores soil productivity to the highest possible level.

- For example, ULM, which is developing the Polokhivske deposit, recently drilled five hydrogeological wells to monitor groundwater properties ‘as part of the International Standards Environmental Impact Assessment (ESIA)’. It also announced the development of a Social Engagement Programme, aiming to ‘maintain openness and mutual understanding between the company… and the local community.’

- The EIA contains two rounds of public consultations, one on the stage of determining the scope of assessment, and the other – after the EIA report. There are no qualification requirements to persons authorised to submit comments and remarks, which, on one hand, provides for inclusion, and on the other, can be used unscrupulously to exert pressure on businesses. The efficiency of the EIA post-implementation monitoring remains questionable.

- Impact assessment of the projects implemented in frontline communities is optional until the end of the martial law. The wartime regime poses additional challenges for civil participation, such as prohibition of protests and limited access to information. Many relevant datasets remain closed for public access, such as the Land Cadastre and the State Geological Survey register of artesian wells.

- This list of minerals is separately defined from the critical raw materials as defined by the EU (see footnote 1), and is far broader, including fossil fuels and most base metals.